A Parent’s Guide to Trump Accounts

Trump Accounts are scheduled to roll out on July 4, 2026, which also happens to be America’s 250th birthday. So naturally, we’ll be celebrating with fireworks, cookouts, and a brand-new IRS account type for children. Apparently, that’s the traditional 250th anniversary gift. Who knew?

So, let’s talk about these big, beautiful Baby IRAs: what they are, how they work, and whether they actually make sense for your family.

What Are Trump Accounts?

At a high level, Trump Accounts are starter retirement accounts for kids.

Parents, grandparents, employers, charities, and certain government entities may be able to contribute while the child is young. But the money cannot be withdrawn until the year the child turns 18. After that, the account starts to look a lot like a traditional IRA.

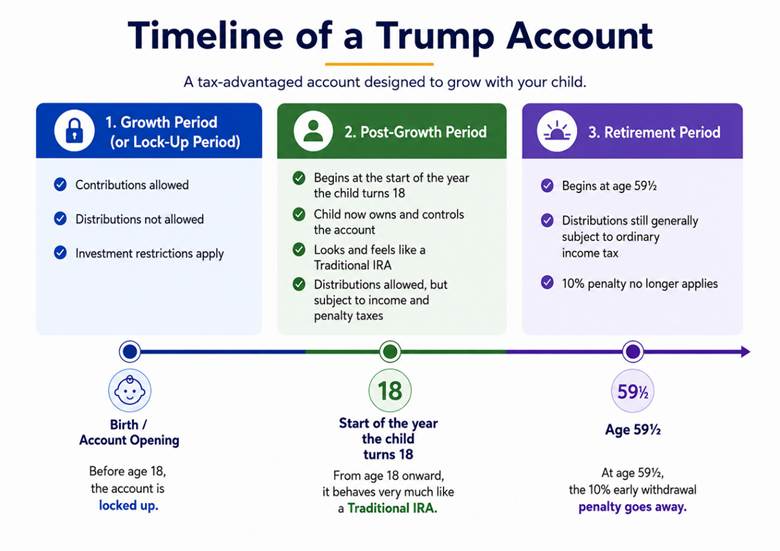

The easiest way to understand Trump Accounts is to think about them in three stages.

Stage 1: The Growth Period — or Lock-Up Period

The first stage runs from the time the account is opened until the beginning of the year the child turns 18.

This period is often called the “growth period,” which makes sense. The money is meant to sit, invest, and compound. But it could just as easily be called the “lock-up period,” because the money generally cannot be accessed at all during this window. That can be a good thing. Forced patience is one of the best ingredients for long-term compounding. But it is also a real limitation.

During the growth period, contributions can come from a few different sources:

- Direct contributions. Parents, grandparents, siblings, or others can contribute to the child’s one Trump Account. These contributions are generally not deductible (after-tax), and the contribution limit is $5,000 per year, indexed for inflation after 2027.

- Employer contributions. Employers may also contribute up to $2,500 per year. This limit is per employee, not per child. So, if an employee has three children, she does not get three separate $2,500 limits. Employer contributions also count toward the same $5,000 combined annual limit, similar to how employer and employee HSA contributions share one overall cap. Unlike direct contributions, employer contributions are made on a pre-tax basis.

- Qualified general contributions. These are contributions made by charities or government entities to specified groups of beneficiaries. These may be less common, but if available, they do not count against the $5,000 direct/employer contribution limit.

- The $1,000 pilot contribution. Eligible children born from 2025 through 2028 can receive a one-time $1,000 contribution. This also does not count against the $5,000 limit.

There are also investment restrictions during the growth period. The account generally has to be invested in qualifying mutual funds or ETFs that track a U.S. equity index. No individual stocks. No international or global funds. No sector-specific funds. No inverse funds. No leveraged funds. No crypto.

So, during this first stage, the setup is pretty simple: money can go in, but it can’t come out.

Stage 2: The Post-Growth Period

The second stage begins on January 1 of the year the child turns 18 (Note: not at the child’s 18th birthday).

At that point, the account starts to function very much like a traditional IRA. Distributions are allowed, Roth conversions are allowed, and the investment restrictions that applied during childhood fall away. The account is also now owned and controlled by the child, not the parent. In practice, the child can generally choose to:

- keep the account designated as a Trump Account,

- roll it into an actual Traditional IRA,

- convert some or all of it to a Roth IRA, or

- take distributions.

The main reason to keep the account designated as a Trump Account instead of rolling it into a traditional IRA is that a standalone Trump Account receives separate basis treatment. In plain English, it does not get lumped together with the owner’s other traditional IRAs for pro-rata tax calculations. That could matter later, especially if the child eventually has other IRA assets or wants to use backdoor Roth IRA contributions.

Because the account is now IRA-like, the usual IRA tradeoffs apply. Withdrawals before age 59½ are generally subject to ordinary income tax and also to a 10% early withdrawal penalty unless an exception applies. So, while the account becomes more accessible after the growth period, it still comes with tax rules and limitations.

This is where it helps to remember that Trump Accounts are not Roth IRAs. Even though direct contributions are made with after-tax dollars (similar to a Roth IRA), the account is much closer to a traditional IRA. In that sense, direct contributions are more like nondeductible contributions to a traditional IRA than Roth IRA contributions. The growth is not tax-free.

Stage 3: The Retirement Period

The third stage begins when the child reaches age 59½.

At that point, the 10% early withdrawal penalty generally goes away, but that doesn’t mean withdrawals are tax-free. Distributions are still taxable to the extent they represent earnings or pre-tax amounts.

This is why Trump Accounts are best understood as retirement accounts first. They may gain some limited flexibility after age 18, but their ideal use is long-term retirement savings. So, this may be a good time to ask your youngster, “When you picture your ideal retirement, what does that look like to you?”

Now that we've covered those stages, you can see the basic lifecycle of a Trump Account:

Should You Use a Trump Account?

Trump Accounts are new and interesting. But they are not “the one account to rule them all.”

The question isn't, “Is this account good?” The better question is, “Good for what?”

Parents already have several ways to save and invest for their children: 529 plans, custodial UTMA accounts, Roth IRAs, and even taxable accounts held in the parents’ names. Trump Accounts are another option in that toolkit, but they are not the best option for every goal.

I’d separate the decision into three parts: free money, your money, and the future strategy for whatever ends up in the account.

Free Money: Take It

This is the easy one.

If your child qualifies for the $1,000 pilot contribution, take it. If your employer offers Trump Account contributions, take them. If your child qualifies for a contribution from a charity or government entity, take that too.

But that does not necessarily mean you should add your own money on top of the free money.

Your Money: Match the Account to the Goal

Once we move beyond free money and ask whether you should add your own contributions to a Trump Account, the planning question becomes more important: what is this money actually for?

If the goal is education, 529 plans are still king. A 529 plan allows money to grow tax-free and come out tax-free when used for qualified education expenses. The rules around qualified expenses are broad, and there are several ways to repurpose leftover 529 funds if your kid doesn’t use all the money for school.

If the goal is flexibility — say you want to help your child save for a first home, a wedding, a business, a car, or just a general “launch fund” — a custodial UTMA account or a parent-owned taxable account is better for that goal. Why are they better? Remember, Trump Accounts are like IRAs, so access from age 18 to 59½ comes with tax consequences--right when many of those various milestones are most likely to happen.

If the goal is retirement, Trump Accounts start to make more sense, although they are still not my first choice. A Roth IRA in the child’s name gets better tax treatment and can be partially accessed tax-free even before 59½. The catch, of course, is that your kid has to have earned income in order to contribute to a Roth IRA. If they don’t, and if you can’t find a creative way for them to earn income, a Trump Account is the next-best option.

Future Strategy: Plan for Roth Conversions

For any money that does end up in a Trump Account, whether from the Treasury, an employer, a charity, or your own contributions, the next planning opportunity is what to do after the growth period ends.

In most cases, the goal should be to strategically convert the Trump Account to Roth over time during the child’s lower-income years. That will likely be during college, early career years, or other years when the child has (relatively) little taxable income.

But this isn’t as simple as “convert the whole thing at age 18.”

The main complication is the kiddie tax. In general, if the child is still young enough to be subject to kiddie tax rules, a large Roth conversion could be taxed at the parents’ tax rate instead of the child’s lower rate. That doesn’t mean Roth conversions are off the table, it just means the conversion strategy should be deliberate. It likely makes sense to convert smaller amounts during kiddie-tax years and then larger amounts once the child is filing independently and still in a low tax bracket.

It's worth noting that conversions are pro rata, meaning if the account contains both after-tax contributions and taxable growth, a conversion includes some of each. Also, there should be a plan for paying the tax. Ideally, conversion taxes would be paid from outside assets, not withheld from the Trump Account itself, which would create additional early-distribution issues, including potential penalty taxes.

So, the Roth conversion strategy can be a great way to optimize Trump Account funds, but the execution matters. At that point, your child controls the account, so the plan will need to involve both of you.

The Practical Takeaway

In summary, I would think about Trump Accounts in three groups:

- Families with access to free money: take it.

- Families already max-funding education and other goals who simply want another tax-advantaged way to transfer wealth to their kids: make direct Trump Account contributions, with a plan to convert to Roth later at low tax rates.

- Everyone else: start with your highest-priority goal, then choose the account that best fits that goal, which may or may not be a Trump Account.

How to Open a Trump Account

If you already filed your 2025 tax return, you may have had a chance to make the Trump Account election with your return. If not, you can also do it online at trumpaccounts.gov.

I went through the online process myself. The website redirected me to an IRS page, and the biggest hurdle was the identity verification step through ID.me. I had to upload a picture of my driver’s license, take a strange, video selfie-type thing, and enter my Social Security number.

Once I got through that, the actual form was easy. I entered my information, entered my kids’ information, and checked the box to elect the $1,000 seed contribution for the kids who qualified. I didn’t receive an immediate email confirmation, which felt a little odd, but the site said confirmation would come later.

For now, these accounts are initially being opened only through BNY Mellon and Robinhood. After submitting the online form, the next step seems to be waiting for activation instructions from Treasury or the custodian. Down the road, they can apparently be rolled over to other custodians if those places support Trump Accounts. So, if you would rather hold the account at Schwab, Fidelity, or somewhere else, that may be an option.

As always, we’re here to help. If you have questions about Trump Accounts or how they may fit into your family’s plan, let us know.